How Much Do You Really Need to Buy a Home in Toronto in 2026?

Jun 07, 2026 11:18 am

Hello!

I want to tell you about a client I worked with and let's call her Jasmine.

She'd been saving for three years. She had $60,000 put away and she was ready to buy. She came to me and said, "Fred, I think I'm finally there."

She wasn't. But she was closer than she thought, and that's the part she wasn't aware of.

Jasmine didn't know about land transfer tax. She didn't know Toronto buyers pay it *twice*, once to the province, once to the city. She didn't know about closing costs, legal fees, or the cash hit from CMHC insurance.

When I laid it all out, she went quiet. Then she asked the question every first-time buyer eventually asks:

"So how much do I actually need?"

That's what this email is about.

---

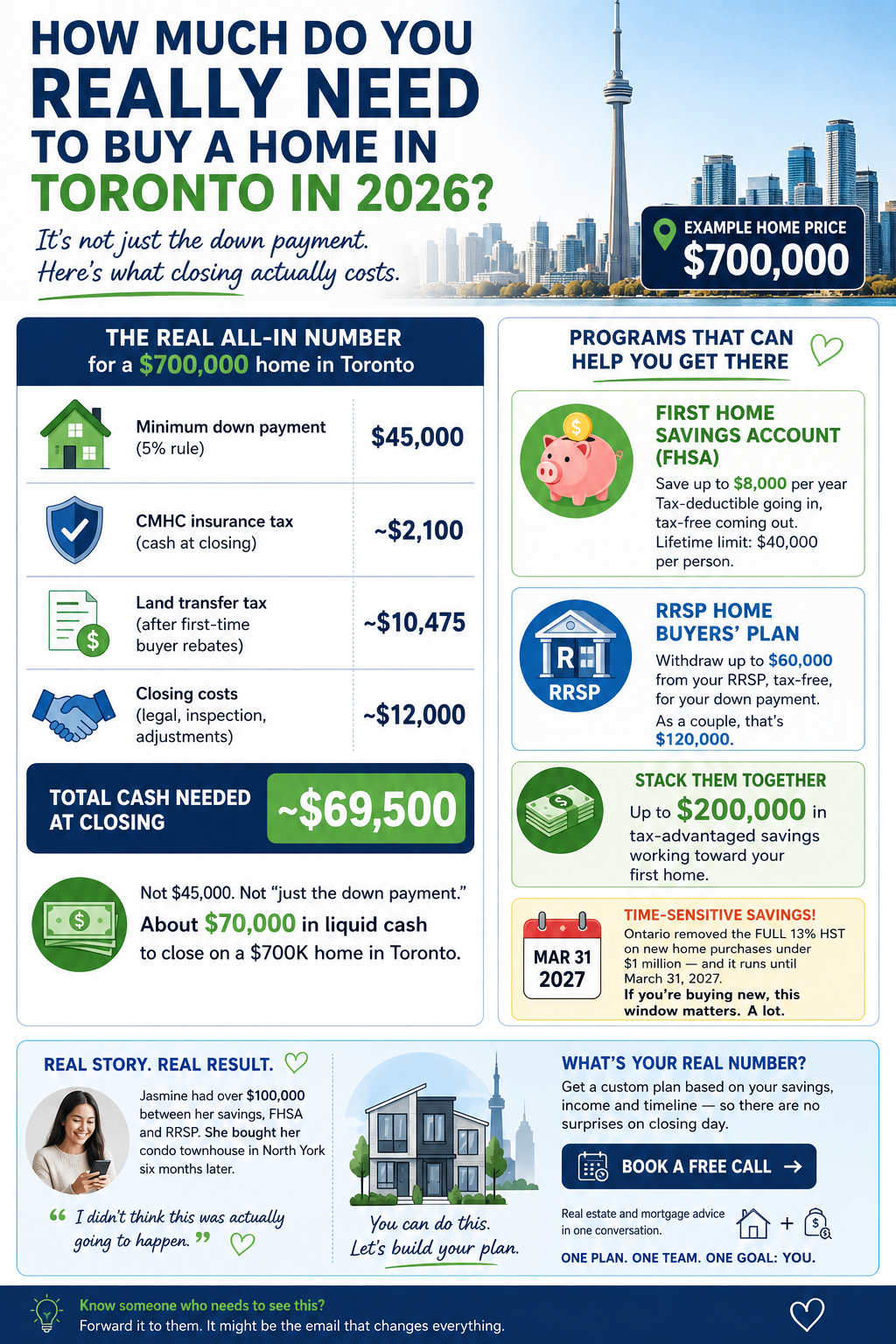

The real all-in number for a $700,000 home in Toronto right now:

Cost Amount

Minimum down payment (5% rule) $45,000

CMHC insurance tax (cash at closing) ~$2,100

Land transfer tax (after first-time buyer rebates) ~$10,475

Closing costs (legal, inspection, adjustments) ~$12,000

**Total cash needed at closing** ~$69,500**

Not $45,000. Not "just the down payment."

About $70,000 in liquid cash to close on a $700K home as a first-time buyer in Toronto.

---

Now here's where it gets better.

There are programs built to help you get there. Most buyers don't know all of them.

The First Home Savings Account (FHSA) lets you save up to $8,000 per year — tax-deductible going in, tax-free coming out. Lifetime limit: $40,000 per person. If you haven't opened one, do it this week.

The RRSP Home Buyers' Plan lets you pull up to $60,000 from your RRSP, tax-free, for your down payment. As a couple, that's $120,000.

Stack them together and you've got up to $200,000 in tax-advantaged savings working toward your first home.

And one more, this one is time-sensitive:

Ontario removed the full 13% HST on new home purchases under $1 million, and it runs until March 31, 2027. If you're looking at a new condo or townhouse, this window matters. A lot.

---

What happened to Jasmine?

Turned out she had her FHSA savings, her RRSP, and her cash all combined, over $100,000. She was ahead of where she thought she was.

She bought a condo townhouse in North York six months later. On closing day she texted me: "I didn't think this was actually going to happen."

That text is why I do this.

___________________________________________

Your next step, if you're ready:

If you want to know your real number, not a guess, a real plan based on your savings, your income, and your timeline. I'm happy to sit down with you.

I'm licensed as both a real estate agent and a mortgage agent. That means you get one conversation that covers the home and the financing. No bouncing between people.

__________________________________________

FOR SALE / FOR LEASE

---

Know someone who needs to see this? Forward it to them. It might be the email that changes everything for them.

______________________________

THE MORTGAGE TRICK YOUR BANK WON'T TELL YOU FIRST

Your mortgage payment is doing less work than you think and here's how to fix that.

Most homeowners make their mortgage payment every month and assume things are moving in the right direction.

They are. Just slowly.

What most people don't realize is that in the early years of a mortgage, the bulk of your payment isn't reducing what you owe it's paying interest. Your balance barely moves. Your bank is happy. But your equity? It's growing at a crawl.

The good news is there are a few simple moves that quietly accelerate that process and most of them don't require you to spend more money every month.

Here's what actually works.

1. Switch from monthly payments to accelerated bi-weekly.

This one move alone can shave years off your mortgage without you ever feeling it. Here's why it works: instead of 12 monthly payments, you end up making the equivalent of 13 in a year. One extra payment annually, spread invisibly across 26 bi-weekly payments. Over a 25-year amortization, that small shift can cut 2 to 3 years off your mortgage and save tens of thousands in interest. Most lenders will set this up with one phone call.

2. Use your prepayment privilege even a little.

Almost every mortgage in Canada comes with a prepayment privilege. That means you're allowed to pay an extra lump sum toward your principal every year. It is usually between 10% and 20% of your original mortgage amount, without any penalty. Even $500 or $1,000 applied directly to your principal has an outsized effect early in your mortgage when interest is front-loaded. You don't have to use it all. Use what you can.

3. Round up your payment.

If your payment is $2,340, pay $2,400. That extra $60 goes straight to your principal, not interest. It sounds small. Over 10 years, it is not small. Small consistent actions on a large balance create results that surprise people when they finally do the math.

4. Be strategic at renewal time.

Most Canadians sign their renewal letter and mail it back without negotiating. That is one of the most expensive things you can do. Your renewal is a leverage moment and your lender wants to keep you, and you have more options than they'll volunteer. The right rate at renewal, combined with the right amortization strategy, can reset your equity-building trajectory entirely. This is exactly where having a mortgage agent in your corner, not just a bank — changes the outcome.

5. Understand what your home's rising value means and doesn't mean.

Equity comes from two places: paying down your mortgage, and your property increasing in value. In the GTA, appreciation has done a lot of the heavy lifting for homeowners over the past decade. But appreciation you can't access isn't money in your pocket, it's money on paper. Understanding how and when to use that equity wisely whether for renovations, investing, or helping your kids into the market is a conversation worth having before you need it, not during.

Here's the honest truth about equity: it builds quietly in the background, and most people only pay attention to it when they're selling or in a financial pinch.

The homeowners who come out ahead are the ones who understand what levers they have and pull them early.

You don't need to be a finance expert to do this. You just need someone to walk you through it in plain language.

Want to know exactly where you stand?

If you're curious how much equity you've built, what your prepayment options are, or whether your current mortgage is still the right fit, let's talk. I'll pull the numbers together and give you a clear picture. No jargon, no sales pitch. Just a straight answer so you can make a confident decision.

Reply to this email and we'll find 20 minutes that work. ☕

Just clarity.

Talk soon,

Fred Camingal